5 Benefits Every Bank VP Should Know About Manufactured Home Loans

September 23, 2016

The fact that manufactured home loans deliver some of the most lucrative investment opportunities is not a secret. However, many categories of investors, including banks and credit unions, are currently missing out on this growing industry segment.

Though we’ve already written several blog posts about the benefits of manufactured home loans for investors, recent market shifts have revealed five new ways a financial institution can benefit from manufactured home lending solutions.

-

Making the most of conventional manufactured home loans

According to a report issued by Enterprise Community Partners and the Harvard Joint Center for Housing Studies, renting has become cost prohibitive for many households. Currently, nearly 12 million families are spending more than 50 percent of their income on rent. Trying to solve the rent increase crisis, certain federal initiatives encourage people to purchase a home instead of renting one. But many would-be home buyers are unable to meet the requirements of government programs. This is where we step in. As our conventional manufactured home financing options don’t come with the amount of rules and regulations that government programs do, adding our loan products to a portfolio means fewer problems for both banks and their customers. In addition, our lending solutions include a series of additional services, such as applicant screening, loan origination and closing procedures, payment processing and collection, cash management, portfolio performance monitoring, borrower communication, compliance and quality control. -

Diversifying across customers

Diversifying a bank’s income streams is a wise choice, irrespective of the economic situation. However, many financial institutions understate the true purpose of diversification. According to experts, a financial institution should seek to diversify not only across asset classes but also across individual customers, particularly if the ability to repay of different categories of consumers presents low correlation. Let’s say that a small bank maintains a greater share of its loan portfolio in agricultural loans. In this case, it may face serious issues if most of its borrowers experience a bad growing season because of poor weather. But if the bank adds manufactured home loans to its portfolio, for example, it will attract a new category of borrowers whose ability to repay won’t be affected by the same adverse events. -

Reducing portfolio risks

Though all consumer and commercial loans exhibit some credit risks, most investors tend to deny these risks instead of trying to identify, manage and avoid them. In addition to performing complex credit analyses, which can help your bank determine the level of risk involved by each category of consumers and loan products, another way to reduce the overall risk of a portfolio is to opt for high-yield, low-risk manufactured home loans. At Triad Financial Services, we provide a variety of manufactured home loan products and services that can help your bank attract new categories of prime borrowers with an average FICO score of 700+ and a low risk of default. -

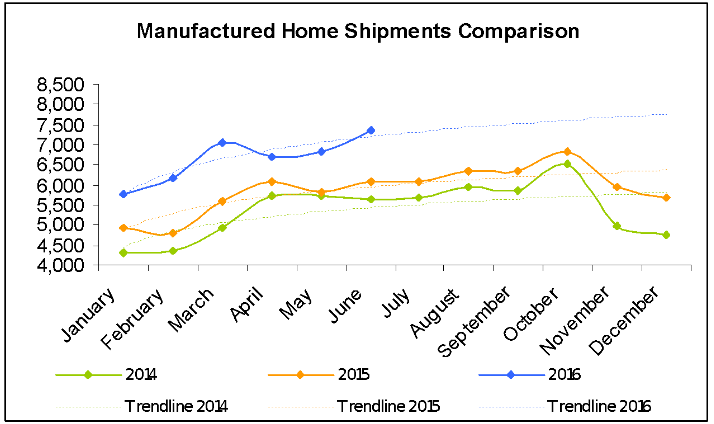

Entering a smaller but prosperous market

After the financial crisis of 2007-2008, investors have started to pay attention to the recovery rate of different industry sectors before making a final investment decision. The good news for the investors showing interest in manufactured home loans – which represent a completely different niche of the home loan industry – is that the manufactured housing industry has recorded significant shipment increases over the past few years. Based on the last report from the MHI, manufactured home shipments have increased by 70 percent since January 2014. -

Going beyond simple diversification

Financial experts argue that investors should diversify their portfolios not only between but also within asset categories. This basically means that a bank should invest in different products that perform differently under certain market conditions. If your bank already offers conventional mortgage products, an effective approach to creating a diversified portfolio would be to opt for manufactured home loans from a well-established, successful manufactured home lender like Triad Financial Services.

After more than half of a century in the manufactured home lending industry, Triad Financial Services is one of the few lenders who offer a full range of manufactured home loan products catering to the needs of investors and comprehensive advisory services relating to credit and borrowing capacity analyses, closing proceedings, collection terms and conditions, asset allocation, portfolio management and performance, and manufactured home retailer selection. To learn more about our products, services and commitment to our partners and customers, we invite you to contact our friendly staff today at (800)-522-2013, Ext. 1287 or investors@triadfs.com.