- Borrowers

- Frequently Asked Questions

Frequently Asked Questions

General Inquiries

Does the home have to be on permanent foundation?

No. We can do singlewide and doublewide homes with or without a permanent foundation. This allows for mobile or manufactured house financing on rental land, in parks, leased property or family land.

What is the maximum loan to value?

Up to 95% LTV on a primary residence purchase. Closing cost can be financed on top of the loan or seller concessions may be used. Credit scores will make the final determination of LTV.

Is Homeowners insurance required and how much?

The borrower must provide proof of one year full coverage at the time of closing. We offer competitive insurance rates. If Triad Financial Services, Inc. policy is accepted, the 1st year's premium can be financed.

Who orders the appraisal, title work, loan closings and etc.?

Triad Financial Services will order all necessary work on the manufactured home loan. We will select the appraiser. The realtor, dealer or the customer may select the title company.

Where do the loans close?

On a home only loan, the realtor / dealer holds the closing, or we will mail the documents directly to you. A notary must notarize several forms. Funds will be disbursed within 48 hours after we receive the closed loan package back in our office. On a land / home loan, all real estate transactions must close with a title company or attorney. Funds will be disbursed at the closing table.

Can the home be purchased through a dealer?

All loan applications must be submitted by a Triad Financial Services, Inc. approved dealer. Please contact the dealership to apply.

What age of a home can be financed?

Age of Home 1976 or newer.

How long does it take between loan application and closing?

Approximately two to three weeks for home-only and four to five weeks for land/home. Our closing department will schedule your loan closing.

What closing fees are charged?

Our closing fees will vary depending on the loan program (home-only vs. land/home) and state the home is located in (state imposed fees). Closing cost can be financed into the loan if necessary.

What about the survey and termite letter?

Triad Financial Services, Inc. does not require a survey or termite letter on the property unless the Title Company is unable to provide title insurance without one. If the customer requests a survey or termite inspection, they must pay for it out of pocket. We will not finance the cost of a survey or termite inspection unless it is a requirement of the Title Company.

Escrow

What is an escrow account?

Think of escrow as a built-in way to spread out your property taxes and insurance so you are not hit with big bills all at once.

Your monthly payment has two parts: one goes toward your loan, and the other goes into your escrow account. When your tax and insurance bills (like homeowners, mortgage, or flood insurance) come due, we pay them for you out of that account.

Check out our educational escrow video to learn more:

How is escrow calculated?

We take your most recent tax and insurance bills, add up the yearly total, and divide by 12 to get your monthly escrow amount.

Example: If your property taxes are about $1,200 a year and your homeowners insurance is $600, that is $1,800 total. Divide by 12, and the escrow part of your monthly payment is $150.

We also keep a small minimum balance (or 'cushion') in your account, up to two months of escrow payments, so you are covered if your taxes or insurance go up.

What is an escrow account cushion?

A cushion is a little extra we keep in your escrow account as a safety net, in case your taxes or insurance go up unexpectedly. It is also the minimum balance your account needs to keep. The cushion amount varies by state, but it can never be more than two months of escrow payments.

What is an escrow account analysis?

At least once a year, we review your escrow account to make sure we are collecting the right amount for your taxes and insurance, since those amounts often change from year to year.

After the review: if your balance is below the minimum required, you will have a shortage; if it is above, you will have an overage.

Want to know what to do about a shortage or overage? See the questions just below.

What is an escrow shortage?

A shortage means your escrow balance has dropped below the minimum required. The most common reason is that your property taxes or insurance premiums went up.

If you have a shortage, see 'How is a shortage collected?' just below for your repayment options.

How is shortage collected?

You have two ways to repay an escrow shortage:

(1) Spread it over 12 months - We divide the shortage across a year and add it to your monthly payment automatically. You do not need to do anything.

(2) Pay it in full - Mail the full shortage amount along with the Escrow Shortage Coupon from your Escrow Analysis Statement. Once we receive it, we remove the shortage amount from your monthly payment.

What is an escrow overage/surplus?

An overage (or surplus) means your escrow balance is above the minimum required. When that happens, we mail a refund check to the address on file, as long as your account is current.

Tip: Make sure your mailing address is up to date so your check reaches you.

Can I use my escrow overage/surplus check toward my monthly payment?

An overage check is refunded to you directly; we are not able to apply it toward your monthly payment. If you would like to put it toward your loan, you can make a separate payment online once you receive your check.

Insurance

What is a Mortgagee Clause?

A mortgagee clause is a standard part of your property insurance that makes sure the insurer will also protect the lender's interest if your home is damaged. In plain terms, it lets your insurer and Triad work together to protect the home.

When your insurer asks for the mortgagee clause, use this:

[Investor Name] ISAOA/ATIMA

C/O Triad Financial Services, Inc.

13901 Sutton Park Drive South, Suite 300

Jacksonville, FL 32224

Does Triad offer insurance products?

Yes. Triad offers affordable insurance for new and used manufactured homes, for homeowners, dealers, and communities. We work with several national carriers, so we can tailor coverage to what you need, including your home, attached structures, personal property, and options like personal liability, guest medical, and loss of use.

You do not need a Triad loan to get coverage from us. Programs include:

- Homeowners insurance

- Dealer coverage (general liability, open-lot inventory)

- Community rentals insurance

For a quote or more information, call our insurance specialists at 1-800-522-2013 x1609.

How much coverage am I required to have?

It depends on the age of your home. Newer and some pre-owned homes are covered at replacement cost, which is what it would cost to replace the home at today's prices. Older homes are covered at actual cash value (ACV), which is the replacement cost minus depreciation (the drop in value over time from normal wear, aging, and similar factors).

Insurance Claim/Loss Draft

What is a loss draft?

A loss draft is the check your insurance company issues after your home is damaged (for example, by a storm). Usually an adjuster inspects the damage first, then once you and your insurer agree on the repair amount, they issue the check, sometimes called a loss draft or claim check. It is made out to both you and Triad Financial Services.

Why is the insurance claim check also made out to Triad?

Because Triad has a shared interest in protecting your home. While you have a loan on the home, both you and Triad have a stake in keeping it in good shape, so insurers make the claim check payable to both of you. This helps make sure the money actually goes toward repairs. It is a normal part of the process, not a sign anything is wrong.

What is the claims process?

Once your home has an insured loss, a Triad Loss Draft Specialist works with you through the whole repair process.

Here's what they handle:

- Getting the details of the damage and the repairs needed;

- Making sure the claim is filed on time;

- Holding any undisbursed funds safely;

- Reviewing and approving the repair plan and bids;

- Checking that completed repairs match the plan; and

- Obtaining lien releases if claim funds pay the loan in full.

We will partner with you from start to finish.

I have damage to my property. What do I do?

First, call your insurance company to file the claim.

Once it is filed and you have your loss draft (claim) check, get in touch with our claims team and we will walk you through the next steps. You can email claims@triadfs.com, or call 1-877-426-8362

What is the claims/loss department’s address?

Mail anything for claims to:

Triad Financial Services

Attn: Claims

13901 Sutton Park Drive South, Suite 300

Jacksonville, FL 32224

You can also email claims@triadfs.com if that is easier.

Taxes

I received a tax bill. Do I send it to you?

Usually not. If your loan has an escrow account, we get your tax bill electronically and pay it for you, so there is nothing to send.

The one exception: if you get a delinquent or corrected tax bill, send us a copy and we will pay it from your escrow account. You can email a clear photo or scan to escrow@triadfs.com, or fax 866-874-2334.

Note: If your loan does not have an escrow account, you are responsible for paying your tax bills yourself.

I received a supplemental/interim tax bill. Do you pay this?

Just log into your account and open your payment history, where you can see any tax payments we have made.

How do I know you paid my taxes?

You can view any tax disbursements by logging into your account and viewing your payment history.

Website Registration

How do I create an online account?

To get started, click the 'Access My Account' link and register.

Tip: Before you begin, clear your browser's cache, cookies, and temporary files, as this prevents most registration issues.

What are the user name requirements?

Your username cannot contain special characters and has to be unique. If you see an 'invalid credentials' message, the name you picked may already be taken, so just try a more unique version.

For example, if 'JSmith' is taken, try 'JSmith12345'.

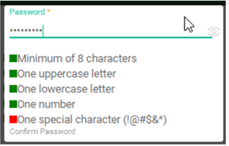

What are the password requirements?

Your password needs to meet the rules shown on screen. When you start typing, each rule shows a red box that turns green once you meet it, so keep going until they are all green.

The special characters you can use are: ! @ # $ & *

Payments

Where can I mail my payment and do I need a coupon?

No coupon needed. Just write your loan number on the check and mail it to:

Triad Financial

P.O. Box 7989

Carol Stream, IL 60197-7989

If you are paying extra, add a note telling us where to apply it (for example, to principal or escrow).

What are my payment options?

You have several ways to pay:

- Autopay (free) - have your payment drafted automatically from your bank account, so you never miss a due date.

- Online - log in and pay anytime.

- Bank bill-pay - use your bank's bill-pay with 'Triad Financial Services' as the payee and your loan number in the notes (allow time, since some banks mail a check).

- Check or money order - include your payment coupon if you get paper statements, and write your loan number on it.

- By phone - pay through an agent at 1-877-426-8362.

Note: Some payment methods may have a fee, but autopay and online payments are free.

Why did my payment change?

The most common reason is your yearly escrow analysis; if your taxes or insurance changed, your payment changes to match (see the Escrow section for the full explanation).

The other common reason is an adjustable-rate mortgage; if your rate is changing, we always mail you a notice beforehand, so it is worth reading any mail from us.

Still not sure? Call 1-877-426-8362.

Why am I not able to pay online?

If the online system will not let you pay, there is usually a specific reason tied to your account (for example, a loan in a special status). A couple of things to try first: make sure you are logged in to the correct loan and that your payment details are current.

If it still will not go through, call 1-877-426-8362 and we will sort it out

Can I cancel my automatic drafting?

Yes. You can cancel autopay, just let us know at least 5 business days before your next scheduled draft date.

How can I pay extra to principal or escrow.

You can pay extra toward principal or escrow online, just log in and choose where you want the extra to go.

If you mail your payment instead, include a note telling us where to apply the additional funds.

Can I pay my loan ahead?

Yes, you can pay your loan ahead by up to three months.

I did not receive my monthly billing statement. How do I pay?

We are here to help, and the sooner we talk, the more options we can explore with you. Please call us at 877-426-8362 so we can find the right path for your situation. Reaching out early is always better than waiting.

I am struggling to make my monthly payments. What do I do?

Call us at (877) 426-8362 so we can assist you with your financial needs.

Payoff Processing

How do I request a payoff statement?

You can request a payoff statement a few ways:

- Online by logging into your account (fastest)

- By email to payoffrequest@triadfs.com

- By fax to 866-874-2334

- By calling an agent at 877-426-8362

If you request it in writing, include a 'good-through' date (within the next 30 days).

I plan to pay off my loan soon, but taxes/insurance are coming due. Will you pay them?

Yes, unless you tell us not to. We will go ahead and pay any upcoming taxes or insurance premiums that come due before your payoff. Keep in mind that if your escrow does not have enough to cover those bills, it can change your final payoff amount. If you would rather we hold off, just let us know.

What happens to my escrow balance after my loan is paid in full?

Any money left in your escrow account is refunded to you within 20 days of payoff. Make sure your mailing address is current so your refund reaches you, you can update it online in your account.

Service Transfers

Why did my loan transfer to Triad?

Loan transfers like this are very common and completely routine. Most importantly, nothing about your loan changes; your terms, balance, and interest rate stay exactly as they were in the documents you originally signed. Triad is simply your new servicer, meaning we are who you will pay and contact going forward.

Will my automatic drafting transfer as well?

Usually not, so you will likely need to set up autopay again directly with Triad. It is quick to do online once your account is registered.

If your autopay did carry over, your servicing transfer notice will say so.

I did not know my account was transferring and made my payment to the prior servicer. What do I do?

No need to worry. Payments made to your previous servicer around the time of transfer are forwarded to Triad, and your account is protected from late fees and negative credit reporting for 60 days after the transfer.

Do I need to update my bill pay service?

Yes. In your bank's bill-pay, change the payee to 'Triad Financial Services' and update the account number to your Triad loan number. That is all it takes to keep your payments flowing to the right place.

%20(1200%20%C3%97%20200%20px).png)