July 13, 2016

The U.S. economy maintains its slow but steady recovery. However, the long-predicted shrinking profit margins as a result of stagnant, or worse, decreasing loan portfolio growth rates have become a reality. Despite loan application volumes remaining constant, there are currently fewer loan closings due to long decision times, prolonged and uncertain approval processes, inadequate or lack of follow-up, increasingly stringent lending guidelines and changing regulatory requirements.

After careful examination of the factors affecting loan portfolio profitability, financial experts have come up with several solutions that can help financial institutions improve the overall efficiency of their portfolios. Below are our top five recommendations along with additional advice you can use to jumpstart your loan portfolio.

Identify underserved market demand.

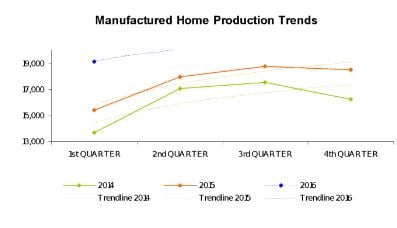

Over the years, investment initiatives in the manufactured home lending sector have been significantly curtailed, partly due to the  regulations limiting the financing options for the consumers seeking small-balance loans for more affordable housing. On the flip side, the newly proposed “duty to serve” rule in conjunction with the increase in demand for decent, affordable dwelling and the recent proliferation of manufactured homes as a viable alternative to site-built housing is expected to turn the “modest” manufactured housing market into one of the fastest-growing sectors with plenty of opportunities for growth. Based on MHI data, growing demand for manufactured homes has positively impacted manufactured home production, shipment and sales volumes, as shown in the chart.

regulations limiting the financing options for the consumers seeking small-balance loans for more affordable housing. On the flip side, the newly proposed “duty to serve” rule in conjunction with the increase in demand for decent, affordable dwelling and the recent proliferation of manufactured homes as a viable alternative to site-built housing is expected to turn the “modest” manufactured housing market into one of the fastest-growing sectors with plenty of opportunities for growth. Based on MHI data, growing demand for manufactured homes has positively impacted manufactured home production, shipment and sales volumes, as shown in the chart.

Analyze applications.

So, you’ve already gathered all the information necessary to determine the financial needs of your target groups of potential borrowers. But what if you’ve missed certain areas? By carefully reviewing the financial situation of your loan applicants and analyzing loan denials, you can identify new investment opportunities. For instance, if you’ve rejected multiple applications because of high DTI ratios, those applicants might have been able to qualify for smaller loans like manufactured home loans.

Focus on new housing trends.

As we have seen in recent news for some time now, consumers are looking for affordable housing. If you just tune into HGTV, you will see everything from tiny houses to revamped manufactured homes being used in affordable housing options. Providing lending options to get qualified candidates the manufactured home loan they need is a growing desire for today's homeowner. Finding the affordable home to meet their needs is highly desired.

Go beyond credit scores.

As a reputable manufactured home lender, we know how important credit scores are when analyzing loan applications. Yet, after nearly 60 years in the manufactured home lending industry, we’ve reached the conclusion that a large number of applications come from people with blemishes on their credit reports, but who have stable jobs and are able to meet their financial obligations. This is the reason why we advise the investors who are looking for ways to jumpstart their loan portfolios to also factor in applicants’ ability to repay the loans, down payment amounts and loan terms in addition to their credit scores.

Conduct a performance analysis.

Another way to boost instead of ”nullifying” organic growth in your loan portfolio this year is to analyze all the lending guidelines your institution has in place: DTI, time on the job, down payment requirements, etc. All lenders base their qualifications on certain criteria applicants must meet in order to qualify for specific loan products. But have you ever analyzed, for a fact, which of your loan approval requirements reduce portfolio risks and potential losses and which ones limit your portfolio growth and profitability? For instance, is there a marked difference between a borrower who has been on his job for 5 years and has a credit score of 740 and a borrower with a 750 FICO credit score, who has only worked for 6 months, provided that both of them have the ability to repay their loans? Can anyone guarantee that the former won’t lose his job next year and default on the loan within several months? Given this scenario, only an exact analysis of your loan portfolio performance data against each lending criterion will tell you which guidelines reduce loss and which ones limit growth.

At Triad Financial Services, our dedicated and experienced professionals can help you implement a wide variety of manufactured home lending strategies, which have been specifically designed to grow loan portfolios. To discuss your investment strategy in more detail, please call our experts today at (800)-522-2013, Ext.-1287 or email investors@triadfs.com.