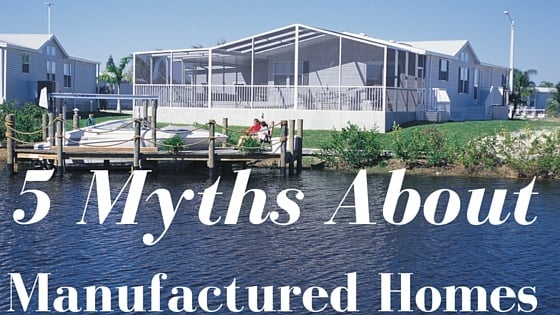

5 Myths About Manufactured Homes

July 28, 2016

Transitioning from renting to buying a home is a major financial decision. As many people are looking for affordable housing options that don’t focus solely on apartment living, could manufactured homes be considered a viable alternative?

Taking into account all the misconceptions surrounding the manufactured housing sector, the answer to this question can’t be a simple “yes” or “no.” To help you make an informed decision, we take this opportunity to address five of the most common myths about manufactured homes.

Myth #1: Manufactured homes are only for low-income families.

When people hear the words “manufactured home,” they tend to envision the old mobile home placed in a trailer park. Modern homes, however, have evolved tremendously from their origins, currently delivering a permanent, durable, and beautiful – sometimes even luxurious – dwelling alternative.

Then why are these homes more affordable than conventional site-built construction? In short, the savings associated with a manufactured home aren’t attributed to lower quality materials but to the efficiencies resulting from the factory-building process.

Assembly-line manufacturing procedures eliminate many of the problems encountered during traditional home construction, including adverse weather conditions, damage to structures/materials, unskilled labor, etc. Since manufactured homes are built with the same or similar building materials as their site-built counterparts, many people who can afford site-built housing decide to buy a manufactured home for different reasons, including price, location, customization options, energy efficiency, etc.

Myth #2: Manufactured homes are difficult to finance.

Financing a manufactured home today is a lot easier than it once was. Though only a handful of lenders offer manufactured home loans, some of them are willing to provide financing options similar to those available for site-built residences. In addition to chattel lending, for instance, Triad Financial Services makes available manufactured home loans with land for both new and used homes. When properly financed, manufactured housing allows homeowners to build equity just as traditional site-built homes.

Myth #3: The HUD Code is less stringent than state or local building codes.

Issued, enforced and monitored by HUD, the Manufactured Housing Program has been developed to safeguard the health and safety of the manufactured home occupants. Under this program, all these homes are built and installed according to the federal building code, also administered by HUD. Compared to the International Residential Code (IRC), HUD code focuses more on performance. However, two comparison studies conducted at the University of Illinois and at the NAHB Research Center have reached the same conclusion, namely that “on balance, the codes are comparable”.

Myth #4: Manufactured homes have poor fire performance properties.

Today's manufactured homes are subject to the same construction and retrofitting standards as traditional site-built houses. A recent study issued by the National Fire Protection Association (NFPA) confirms that a manufactured home built to HUD standards have similar fire-resistance characteristics to any other site-built residence.

Myth #5: There is no inspection system in place for manufactured homes.

Not only does HUD regulate the design, construction, quality, transportability, durability, fire resistance and energy efficiency of the manufactured homes; it also monitors the compliance with the federal building code. Under the HUD program, state and third-party agencies check and approve designs, materials, manufacturing and installation procedures to ensure that each manufactured home complies with the pre-approved standards. HUD has also started to review manufactured home installation manuals in order to eliminate confusion susceptible to individual interpretations and ensure consistency in the manufacturing and installation practices.

One final piece of advice: Don’t rule out the alternative offered by the manufactured housing sector based solely on what you read online. Instead, get in touch with a team of reliable and reputable professionals who have extensive experience in this industry, ask your questions and analyze every aspect of information carefully before making your final decision. For expert advice on any matter relating to manufactured home financing, feel free to contact our dedicated professionals today at (800)-522-2013.